The July US jobs report will spherical out a busy week for market members with, as is typical, the primary Friday of the month bringing the most recent learn on circumstances inside the US labour market.

After the June report confirmed a cooling within the jobs market, the July information is more likely to observe swimsuit, pointing to a continued normalisation in circumstances, cementing the case for a September Fed minimize.

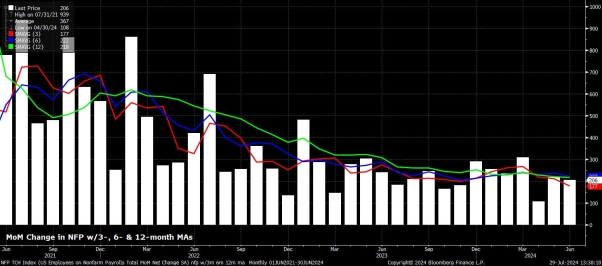

Headline nonfarm payrolls are set to have risen by +178k in July, a contact beneath the +206k tempo seen in June (pending revisions), and broadly consistent with the 3-month common of job positive factors at +177k, although this common presently resides at its lowest degree because the starting of 2021.

Whereas the vary of estimates, at +70K to +225k, is often huge, a print inside this band would nonetheless represents a tempo of job creation that is still a way beneath the ‘breakeven’ payrolls tempo, of round +250k, required for employment development to maintain tempo with development within the dimension of the labour drive.

Given the timing of this month’s labour market report, a few of the regular main indicators, such because the ISM PMI surveys, aren’t accessible on the time of writing, shan’t have been launched by the point the BLS unveil the roles information on Friday.

However, one may argue that dangers to the NFP consensus are marginally biased to the draw back, primarily owing to the unsure affect of Hurricane Beryl on employment, with the storm having made landfall within the USA in the course of the survey week. It will, possible, have extra of a adverse affect on the institution survey, than on the family survey metrics.

In the meantime, preliminary jobless claims remained largely unchanged between the June and July survey weeks, although persevering with claims did rise +19k over that interval, and stay near the highest degree since 2021.

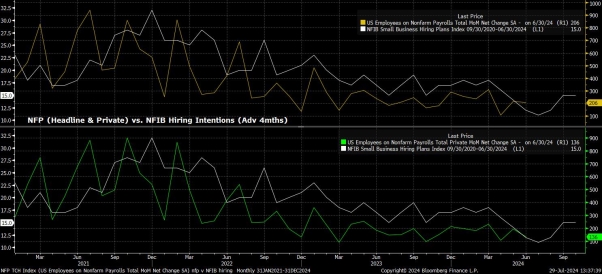

The newest NFIB hiring intentions survey additionally factors to potential draw back dangers for the payrolls print, and has been a remarkably correct indicator, notably of personal payrolls development, this cycle. For each personal, and headline, job creation, the NFIB survey factors to an increase of round +100k, proper in the direction of the underside of the aforementioned forecast vary.

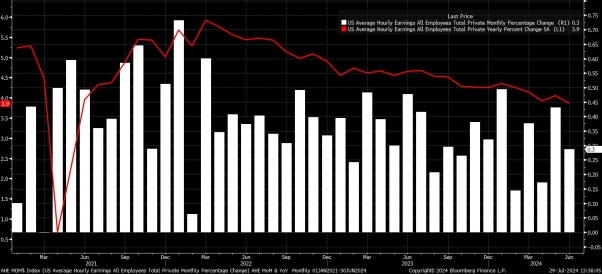

Sticking with the institution survey, common hourly earnings are set to have risen by 0.3% MoM in July, unchanged from the tempo seen a month prior. On an annual foundation, owing largely to base results from 2023’s information, this could see earnings development cool to three.7% YoY, down 0.2pp on the tempo seen in June.

Clearly, such a cooling in annual earnings development, even when partly owing to statistical quirks, can be welcomed by FOMC policymakers, whereas additionally representing a continued cooling in wage pressures, and a price of earnings development that’s changing into more and more suitable with a sustainable return to the two% inflation goal over the medium time period. In flip, such information ought to present the FOMC with additional ‘confidence’ that price cuts can quickly be delivered.

Turning to the family survey, headline unemployment is anticipated to stay unchanged at its highest degree since November 2021, at 4.1%, within the July jobs report, whereas labour drive participation must also maintain regular at 62.6%, marginally beneath the cycle highs seen in the midst of 2023.

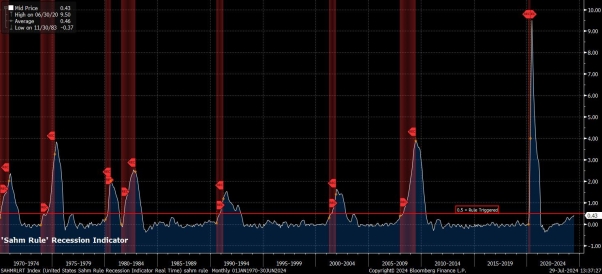

Nonetheless, it’s value noting {that a} rise in joblessness to 4.2% would consequence within the so-called ‘Sahm Rule’ being triggered as, in such an occasion, the 3-month transferring common of unemployment would then have risen by 0.5pp from the 12-month low.

Whereas no financial indicator, or sign, is foolproof, the ‘Sahm Rule’ has been famous for its accuracy, having been triggered prematurely of each US recession since 1970. That mentioned, with US GDP having grown by an annualised tempo of over 2% in 7 of the final 8 quarters, perhaps this cycle is the one when the rule will likely be damaged.

Zooming out, it appears unlikely that the July jobs report will likely be a game-changer by way of the FOMC coverage outlook, although in fact that is mentioned pending feedback from the Committee on Wednesday, the place the assertion, and post-meeting press convention, ought to each lay the groundwork for a 25bp minimize in September.

Whereas a hotter-than-expected print, notably by way of the earnings part, might spark some concern in regards to the potential stubbornness of worth pressures, such information would possible not be sufficient to discourage the FOMC from starting to normalise coverage sooner slightly than later, given a reluctance to over-react to at least one single information level, and a longstanding view that inflation returning to focus on doesn’t require substantial labour market weak point.

Then again, cooler-than-expected information would merely match with the broader theme of current jobs information, representing an extra gradual and regular cooling of labour market circumstances, and sure additional cementing the case for a minimize on the subsequent FOMC assembly in September.

For monetary markets, nevertheless, the roles report will possible as soon as extra show a big vol occasion, with members set to view the figures by the lens of the longer-run coverage outlook, and the cumulative easing that the FOMC are more likely to ship this 12 months. Right here, upside USD dangers current themselves, with the OIS curve discounting over 65bp of cuts – i.e., implying a 60% likelihood of 3x 25bp cuts this 12 months – by the top of December. Such a tempo appears significantly extra speedy than the FOMC would possible ship, therefore mentioned cuts are more likely to be priced out, sparking some USD demand within the course of, over the medium-run.

The July US jobs report will spherical out a busy week for market members with, as is typical, the primary Friday of the month bringing the most recent learn on circumstances inside the US labour market.

After the June report confirmed a cooling within the jobs market, the July information is more likely to observe swimsuit, pointing to a continued normalisation in circumstances, cementing the case for a September Fed minimize.

Headline nonfarm payrolls are set to have risen by +178k in July, a contact beneath the +206k tempo seen in June (pending revisions), and broadly consistent with the 3-month common of job positive factors at +177k, although this common presently resides at its lowest degree because the starting of 2021.

Whereas the vary of estimates, at +70K to +225k, is often huge, a print inside this band would nonetheless represents a tempo of job creation that is still a way beneath the ‘breakeven’ payrolls tempo, of round +250k, required for employment development to maintain tempo with development within the dimension of the labour drive.

Given the timing of this month’s labour market report, a few of the regular main indicators, such because the ISM PMI surveys, aren’t accessible on the time of writing, shan’t have been launched by the point the BLS unveil the roles information on Friday.

However, one may argue that dangers to the NFP consensus are marginally biased to the draw back, primarily owing to the unsure affect of Hurricane Beryl on employment, with the storm having made landfall within the USA in the course of the survey week. It will, possible, have extra of a adverse affect on the institution survey, than on the family survey metrics.

In the meantime, preliminary jobless claims remained largely unchanged between the June and July survey weeks, although persevering with claims did rise +19k over that interval, and stay near the highest degree since 2021.

The newest NFIB hiring intentions survey additionally factors to potential draw back dangers for the payrolls print, and has been a remarkably correct indicator, notably of personal payrolls development, this cycle. For each personal, and headline, job creation, the NFIB survey factors to an increase of round +100k, proper in the direction of the underside of the aforementioned forecast vary.

Sticking with the institution survey, common hourly earnings are set to have risen by 0.3% MoM in July, unchanged from the tempo seen a month prior. On an annual foundation, owing largely to base results from 2023’s information, this could see earnings development cool to three.7% YoY, down 0.2pp on the tempo seen in June.

Clearly, such a cooling in annual earnings development, even when partly owing to statistical quirks, can be welcomed by FOMC policymakers, whereas additionally representing a continued cooling in wage pressures, and a price of earnings development that’s changing into more and more suitable with a sustainable return to the two% inflation goal over the medium time period. In flip, such information ought to present the FOMC with additional ‘confidence’ that price cuts can quickly be delivered.

Turning to the family survey, headline unemployment is anticipated to stay unchanged at its highest degree since November 2021, at 4.1%, within the July jobs report, whereas labour drive participation must also maintain regular at 62.6%, marginally beneath the cycle highs seen in the midst of 2023.

Nonetheless, it’s value noting {that a} rise in joblessness to 4.2% would consequence within the so-called ‘Sahm Rule’ being triggered as, in such an occasion, the 3-month transferring common of unemployment would then have risen by 0.5pp from the 12-month low.

Whereas no financial indicator, or sign, is foolproof, the ‘Sahm Rule’ has been famous for its accuracy, having been triggered prematurely of each US recession since 1970. That mentioned, with US GDP having grown by an annualised tempo of over 2% in 7 of the final 8 quarters, perhaps this cycle is the one when the rule will likely be damaged.

Zooming out, it appears unlikely that the July jobs report will likely be a game-changer by way of the FOMC coverage outlook, although in fact that is mentioned pending feedback from the Committee on Wednesday, the place the assertion, and post-meeting press convention, ought to each lay the groundwork for a 25bp minimize in September.

Whereas a hotter-than-expected print, notably by way of the earnings part, might spark some concern in regards to the potential stubbornness of worth pressures, such information would possible not be sufficient to discourage the FOMC from starting to normalise coverage sooner slightly than later, given a reluctance to over-react to at least one single information level, and a longstanding view that inflation returning to focus on doesn’t require substantial labour market weak point.

Then again, cooler-than-expected information would merely match with the broader theme of current jobs information, representing an extra gradual and regular cooling of labour market circumstances, and sure additional cementing the case for a minimize on the subsequent FOMC assembly in September.

For monetary markets, nevertheless, the roles report will possible as soon as extra show a big vol occasion, with members set to view the figures by the lens of the longer-run coverage outlook, and the cumulative easing that the FOMC are more likely to ship this 12 months. Right here, upside USD dangers current themselves, with the OIS curve discounting over 65bp of cuts – i.e., implying a 60% likelihood of 3x 25bp cuts this 12 months – by the top of December. Such a tempo appears significantly extra speedy than the FOMC would possible ship, therefore mentioned cuts are more likely to be priced out, sparking some USD demand within the course of, over the medium-run.

{kind=link}