Summer season markets’ seem to have arrived, a time characterised by skinny volumes, and comparatively low volatility; traits that ought to permit markets to proceed to take the ‘path of least resistance’, barring any surprising exogenous shocks.

With out wishing to doubtlessly jinx issues, it might seem that ‘summer time markets’ at the moment are effectively and really upon us.

Barring a quick bout of volatility stemming from finish of month/quarter/half-year flows, market motion of late has been akin to watching paint dry.

With the financial calendar remaining comparatively barren till subsequent Friday’s US jobs report – which, after all, coming a day after Independence Day, will drop when few individuals are at their desks – this relative calm seems like it might persist for a while to return.

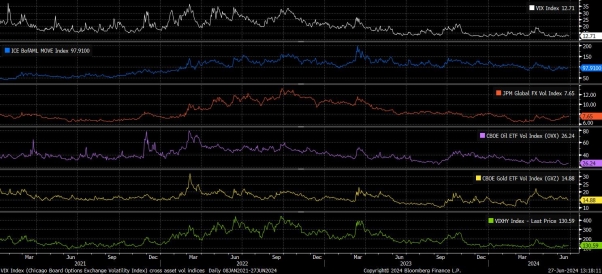

To place some figures with the above, implied vols throughout all main asset courses stay at extremely low ranges. The VIX continues to commerce with a 12 deal with, simply inches above the cycle lows seen a few weeks in the past, whereas BofAML’s MOVE index of Treasury vol additionally stays subdued, with related cycle low, or close to cycle low, ranges of implied vol additionally being seen in each gold, and crude.

The FX market has, on the headline degree, considerably bucked this pattern, with JPM’s international FX vol index buying and selling at a 2-week excessive 7.65, not far off its highest ranges this 12 months. The overwhelming majority, nevertheless, of this latest rise has stemmed from a rise in EUR vols, on account of rising political uncertainty throughout the bloc. Elsewhere in G10, implieds stay beneath the 25th %ile of respective 52-week ranges.

Not solely has implied vol fallen, however realised has additionally.

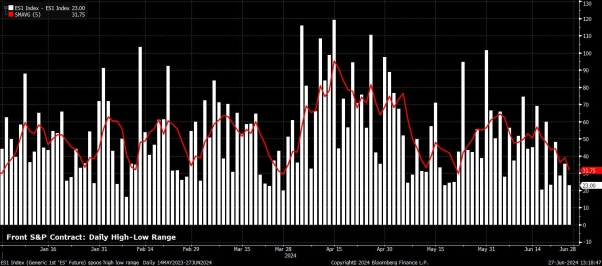

CBOE’s RVOL index, for instance, trades at its lowest degree of the 12 months, and actually its lowest since Fed Chair Powell’s dovish pivot final December. In the meantime, the high-low every day vary within the entrance S&P 500 future continues to tighten, with the 5-day shifting common of mentioned vary now a meagre 31 factors, the narrowest in a couple of month.

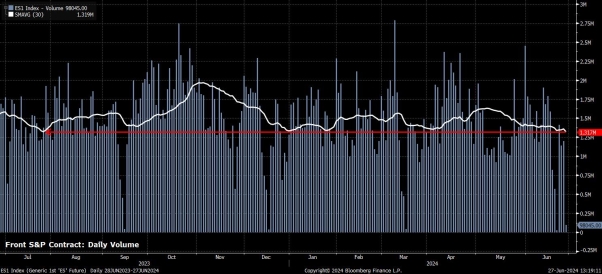

As implied and realised vol have declined, so have buying and selling volumes.

Within the entrance S&P 500 future, the 30-day common of every day quantity now stands at round 1.3mln contracts, the bottom such degree since final July. Comparable is seen within the money market, the place every day quantity is usually working at round 10-15% beneath the 20-day common.

Maybe most significantly, this all begs the query of how market individuals can adapt to those buying and selling situations, which – if latest years are something to go by – are more likely to persist till Labor Day in early-September.

Firstly, it’s vital to recognise that whereas situations could also be quiet, and liquidity thinner than traditional, this doesn’t essentially imply that markets will tread water all the time. Had been an surprising headline, or vastly out-of-consensus knowledge level, to cross information wires, the market response to mentioned knowledge is more likely to be way more vital than in ‘typical’ occasions, owing to considerably fewer than traditional individuals participating with markets. Naturally, correct danger administration ought to turn out to be much more of a precedence than traditional on this kind of an setting.

In addition to this, you will need to adapt one’s expectations for the diploma of (or, lack of) market motion that’s more likely to be seen. Implied vols are of explicit use right here, on condition that one is ready to extrapolate – to each one and two customary deviations of confidence – an asset’s seemingly buying and selling vary from mentioned data. An instance of this for FX majors, is beneath.

General, nevertheless, the shortage of volatility, mild volumes, and certain mild news- and data-flow, ought to all mix to see markets persevering with to take the ‘path of least resistance’ over the medium-term.

As has been the case for a while, mentioned path continues to level to the upside for equities, albeit with the upcoming Q2 earnings season a danger, with development remaining resilient, and the ‘Fed put’ set to supply extra help. Elsewhere, Treasuries appear more likely to stay inside a spread till larger readability on the timing of the primary Fed minimize is obtained, a base case which additionally applies to the greenback, as divergences between G10 central banks stay comparatively slender.

Summer season markets’ seem to have arrived, a time characterised by skinny volumes, and comparatively low volatility; traits that ought to permit markets to proceed to take the ‘path of least resistance’, barring any surprising exogenous shocks.

With out wishing to doubtlessly jinx issues, it might seem that ‘summer time markets’ at the moment are effectively and really upon us.

Barring a quick bout of volatility stemming from finish of month/quarter/half-year flows, market motion of late has been akin to watching paint dry.

With the financial calendar remaining comparatively barren till subsequent Friday’s US jobs report – which, after all, coming a day after Independence Day, will drop when few individuals are at their desks – this relative calm seems like it might persist for a while to return.

To place some figures with the above, implied vols throughout all main asset courses stay at extremely low ranges. The VIX continues to commerce with a 12 deal with, simply inches above the cycle lows seen a few weeks in the past, whereas BofAML’s MOVE index of Treasury vol additionally stays subdued, with related cycle low, or close to cycle low, ranges of implied vol additionally being seen in each gold, and crude.

The FX market has, on the headline degree, considerably bucked this pattern, with JPM’s international FX vol index buying and selling at a 2-week excessive 7.65, not far off its highest ranges this 12 months. The overwhelming majority, nevertheless, of this latest rise has stemmed from a rise in EUR vols, on account of rising political uncertainty throughout the bloc. Elsewhere in G10, implieds stay beneath the 25th %ile of respective 52-week ranges.

Not solely has implied vol fallen, however realised has additionally.

CBOE’s RVOL index, for instance, trades at its lowest degree of the 12 months, and actually its lowest since Fed Chair Powell’s dovish pivot final December. In the meantime, the high-low every day vary within the entrance S&P 500 future continues to tighten, with the 5-day shifting common of mentioned vary now a meagre 31 factors, the narrowest in a couple of month.

As implied and realised vol have declined, so have buying and selling volumes.

Within the entrance S&P 500 future, the 30-day common of every day quantity now stands at round 1.3mln contracts, the bottom such degree since final July. Comparable is seen within the money market, the place every day quantity is usually working at round 10-15% beneath the 20-day common.

Maybe most significantly, this all begs the query of how market individuals can adapt to those buying and selling situations, which – if latest years are something to go by – are more likely to persist till Labor Day in early-September.

Firstly, it’s vital to recognise that whereas situations could also be quiet, and liquidity thinner than traditional, this doesn’t essentially imply that markets will tread water all the time. Had been an surprising headline, or vastly out-of-consensus knowledge level, to cross information wires, the market response to mentioned knowledge is more likely to be way more vital than in ‘typical’ occasions, owing to considerably fewer than traditional individuals participating with markets. Naturally, correct danger administration ought to turn out to be much more of a precedence than traditional on this kind of an setting.

In addition to this, you will need to adapt one’s expectations for the diploma of (or, lack of) market motion that’s more likely to be seen. Implied vols are of explicit use right here, on condition that one is ready to extrapolate – to each one and two customary deviations of confidence – an asset’s seemingly buying and selling vary from mentioned data. An instance of this for FX majors, is beneath.

General, nevertheless, the shortage of volatility, mild volumes, and certain mild news- and data-flow, ought to all mix to see markets persevering with to take the ‘path of least resistance’ over the medium-term.

As has been the case for a while, mentioned path continues to level to the upside for equities, albeit with the upcoming Q2 earnings season a danger, with development remaining resilient, and the ‘Fed put’ set to supply extra help. Elsewhere, Treasuries appear more likely to stay inside a spread till larger readability on the timing of the primary Fed minimize is obtained, a base case which additionally applies to the greenback, as divergences between G10 central banks stay comparatively slender.

{kind=link}